CHARLOTTE — For the second time this year, the Federal Reserve has raised the interest rate by a half-percentage point, which is the largest hike since 2000.

For many people, it means they will be paying more interest when they borrow money on credit cards, car loans, home equity loans and mortgages.

Shayna Whitman dreams of home ownership. She says her interest rates have been jumping so much already that within two weeks, interest rates did go up 0.5%, “which makes a huge difference in your monthly mortgage payment.”

She bought a house and locked in a rate months before she planned to. “I’m trying to feel confident and just stay positive about it … It’s hard. We work really hard for our money,” she told Action 9′s Jason Stoogenke. “Am I going to still be able to afford this home?”

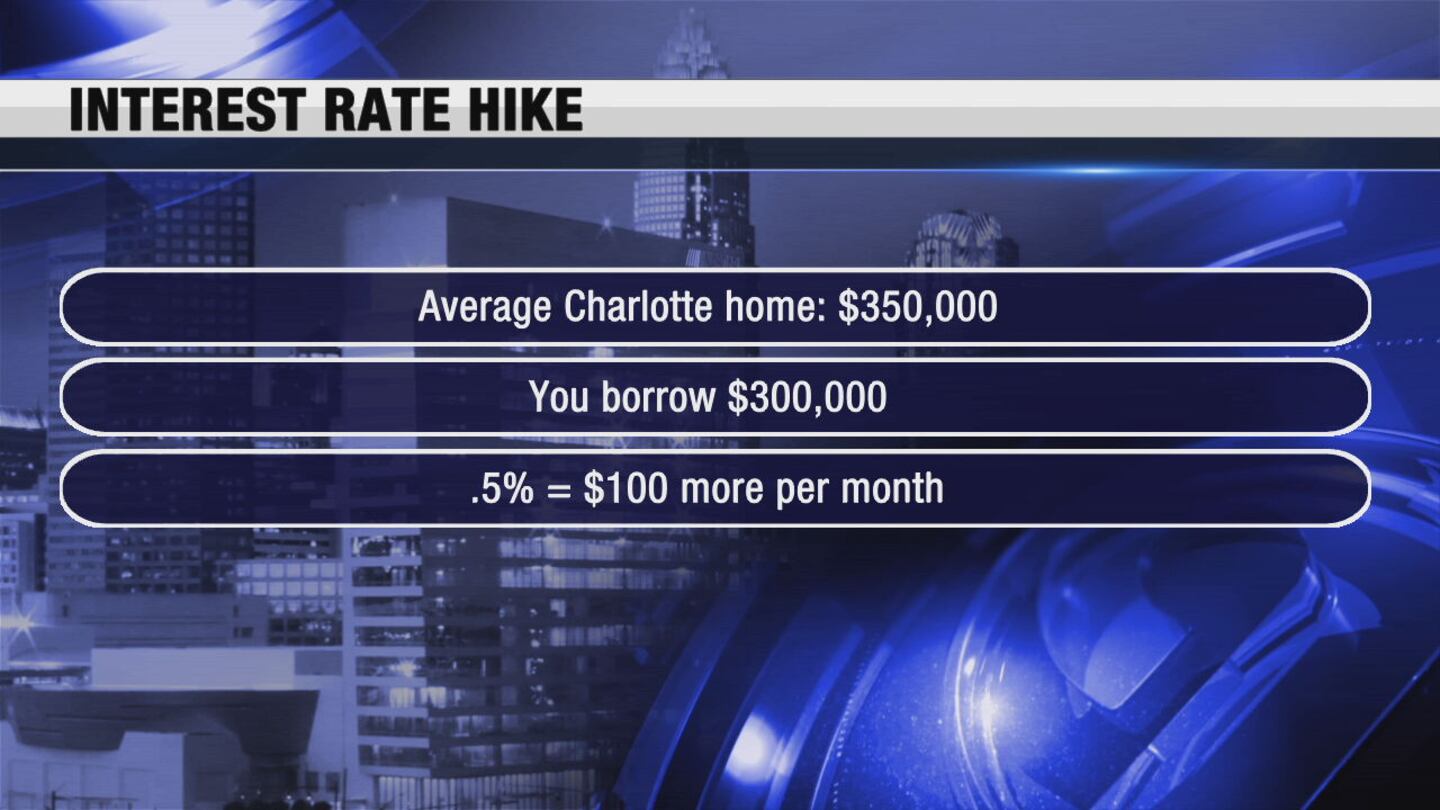

Analysts say the average Charlotte home is $350,000, so if someone borrowed $300,000, they would owe about $100 more each month.

“The real story here is, prepare for a sustained period of these interest rate hikes,” Ted Rossman with Bankrate.com told Stoogenke. “If the trend continues, by the end of the year, it wouldn’t be surprising for mortgage rates to be, let’s say 6%.” (A 30-year mortgage is currently 5.25%.)

If your rate is already locked in on a mortgage or car loan, the hike does not impact you. But it does affect you if you borrow money in the future or carry debt on your credit card.

(WATCH BELOW: Spending a lot on rental application fees? Here’s one way to save money)

©2022 Cox Media Group

/cloudfront-us-east-1.images.arcpublishing.com/cmg/LH3JSJEF3VBLRJLJQESEAG34AM.png)